This article was written with accurate, fact—checked research conducted day Ai. As a writer, I am so happy to have more time to ideate vs research! I assure you, these thoughts and conclusions belong to me. If you missed long form content that is well researched then this article is for you. Please read and let me know your thoughts!

If you’ve spent years plotting your season around Las Vegas, Paris, Copenhagen, or Denver, it can feel like the ground shifted under your feet. Some long-standing fashion and apparel trade shows are drawing smaller crowds than before, discovery now happens on Instagram and TikTok in real time, and the DTC era recalibrated the value of wholesale-centric forums. Yet the truth on the show floor is more nuanced: attendance at many B2B exhibitions remains below 2019, but buyers and exhibitors are coming back where value is unmistakable—especially when organizers redesign around curated matchmaking, hands‑on demos, and community moments that feel real rather than manufactured. In other words, we aren’t seeing a funeral for trade shows; we’re seeing a forced evolution, and the winners are already writing the rules for the next decade. CEIR1 TSNN2 nrf.com3

What’s really shifting: DTC, wholesale, and the changing job of a show

The last decade’s direct‑to‑consumer boom reduced dependence on wholesale for many brands; that alone made “meet all your buyers in one hall” less central to some go‑to‑market plans. But even DTC champions are now rebalancing. In 2024, Nike explicitly “leaned back into wholesale,” calling out the importance of serving consumers in multibrand retail and making reinvestment in wholesale partners one of four strategic priorities—backed by results like 8% currency‑neutral wholesale growth in fiscal Q4 and 2% wholesale growth for the year. Adidas’s turnaround similarly rode a wholesale rebound—up 13% currency‑neutral in Q3 2024—with faster wholesale growth and improvement in the U.S. called out by business press. The implication for trade shows: they’re still relevant—just not by default. They must prove they’re the most efficient way to unlock incremental wholesale reach, content, or collaboration you can’t replicate in an algorithmic feed. Retail Dive4 investors.nike.com5PYMNTS6 adidas-group.com7 Bloomberg8

The age of social discovery changed who holds the mic—and when

It’s never been easier for brands to reach end customers (and peers) without a badge. In TikTok’s own 2024 Shopping Trend report, users said they’re 5.2x more likely to see TikTok as the best platform to connect with brands versus other social/video platforms; nearly half keep researching a product on TikTok after discovering it there. Instagram sits atop product discovery: Sprout Social’s 2024 content study found 61% of social users turn to Instagram to find their next purchase, and other compendia peg “shopping enthusiasts” even higher. The result is a flood of trend talk, “how‑to” explainers, and self‑proclaimed gurus who can publish hours after a runway moment—info that once lived behind an event badge. That doesn’t make shows obsolete; it raises the bar. To justify the trip, shows need knowledge, access, and serendipity you can’t scroll past on your phone. TikTok Ads9 Sprout Social10HubSpot Blog11

Are trade shows actually shrinking? The data says “recovering, but uneven”

At the macro level, the U.S. B2B exhibition industry is still climbing back: CEIR’s Q4 2024 Total Index was 4.4% below the same quarter in 2019—an improvement from a 10.9% shortfall a year earlier. Under the hood, exhibit space has recovered the fastest (net square feet just 2.7% below 2019 in Q3 2024), exhibitor counts lag more modestly (down ~7%), and attendance is the slowest to return (still ~17.8% below Q3 2019), reflecting lingering travel budgets and changing attendee calculus. Globally, UFI’s Barometer has shown robust revenue recovery across organizers, even as attendee dynamics vary by region and vertical. Translation: shows aren’t “dead,” but they can’t assume pre‑2020 attendance behavior will simply snap back without rethinking value delivery. CEIR1 TSNN2 UFI12

Concrete examples: where attendance fell, where it surged, and what made the difference

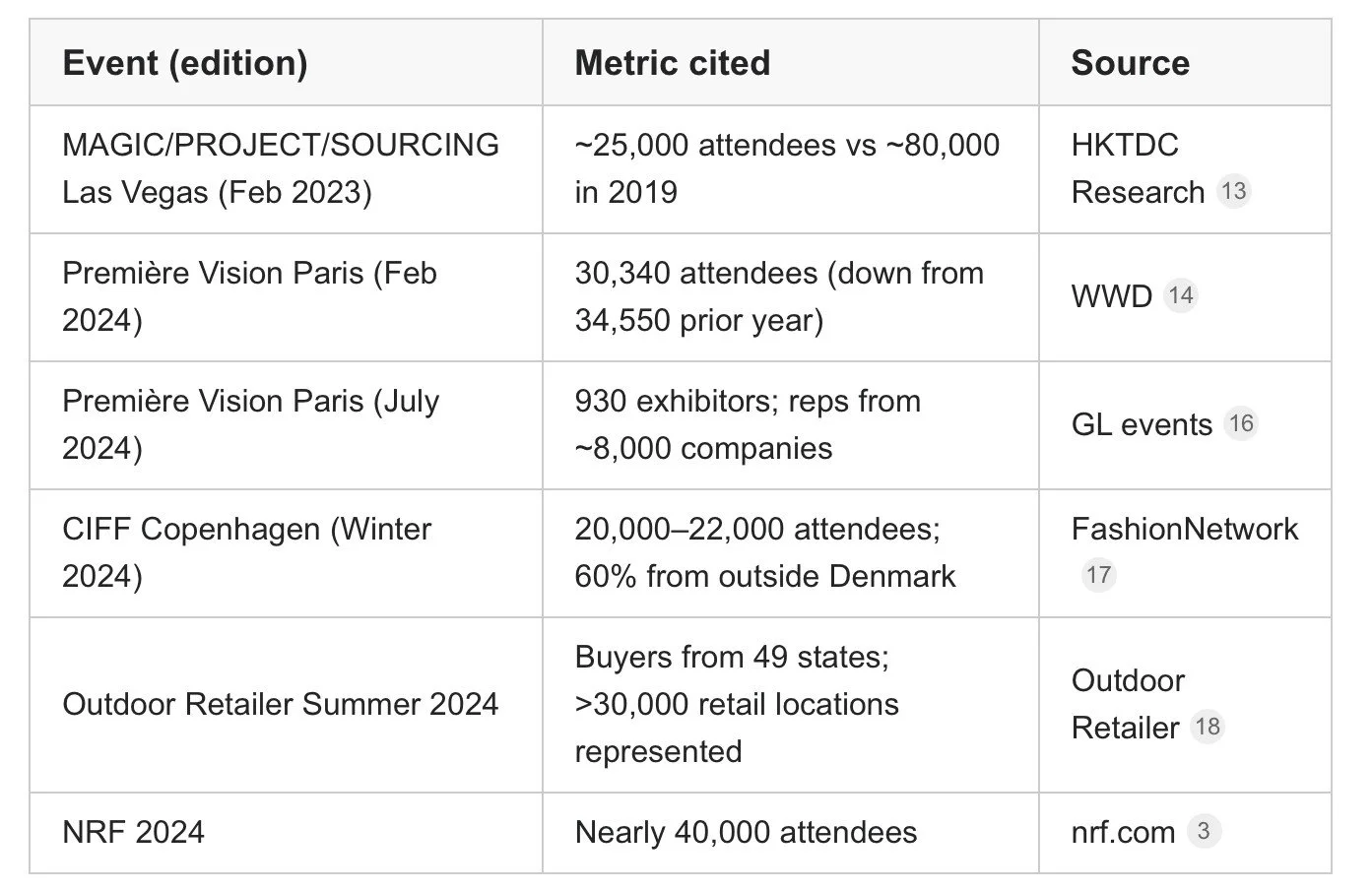

MAGIC Las Vegas: The co‑located MAGIC/PROJECT/SOURCING events have reduced to a tighter footprint post‑pandemic. One snapshot from early 2023 put overall attendance at about 25,000 versus roughly 80,000 in 2019, even as organizers reported an 8% uptick over the prior year and 30% more new exhibitors—evidence of an event in transition, with improving sentiment but a smaller headcount. HKTDC Research13

Première Vision Paris: The February 2024 edition drew 30,340 visitors from 125 countries, down from 34,550 the prior year, but exhibitors called the footfall “more substantial,” emphasizing meeting quality and stand frequency over raw volume; by July 2024, PV reported 930 exhibitors from 40+ countries and representatives from nearly 8,000 companies, signaling buyer depth even with tighter totals. WWD14 The Spin Off15 GL events16

CIFF Copenhagen: A counterexample of momentum—winter edition reports indicated a sharp rise to 20,000–22,000 attendees, 60% pre‑registered from outside Denmark, and growing pull from Germany, Asia, and Canada, propelled by the Revolver integration and a strong sustainability/editorial lens. FashionNetwork17

Outdoor Retailer: The summer 2024 edition leaned into hosted buyers, dedicated buyer hours, and a new sourcing show; buyers represented more than 30,000 retail locations with a 3:1 buyer‑to‑brand ratio—less a “traffic” story than a pipeline‑quality one that exhibitors can monetize. Outdoor Retailer18

NRF: Retail’s Big Show remains an outlier in scale—it drew “nearly 40,000” attendees in 2024, buoyed by agenda breadth (AI, supply chain, loyalty), side events, and the density of decision‑makers shopping for transformation, not just product. For fashion‑adjacent brands, NRF’s draw shows how a strong content thesis plus buyer curation can hold or grow attendance in a tough cycle. nrf.com3Pivotree19

Table: A quick snapshot of cited event metrics

The networking question after COVID: did we lose the urge to connect?

COVID did a number on everyone, and some folks became more selective about crowds. But the recovery story is more “recalibration” than retreat. Freeman’s large 2024 study reports 82% of respondents prefer in‑person events over online, 92% expected to attend more in‑person events in the next 12 months, and in‑person remains the most trusted channel in the marketing mix. The catch: attendees are laser‑focused on return for time and budget—87% say discovering new products/solutions is the top factor in deciding to attend, with hands‑on demos, expert access, and curated agendas among the highest‑value features. That squares with what we hear on the floor: willingness to travel is back when the agenda and meetings feel indispensable, but “just okay” programming won’t pry people from production calendars and social feeds. Freeman press20 Freeman report PDF21

The “Instagrammable moment” trap—and how to design experiences that actually work

Attendees want stimulation, but they can smell contrived spectacles. Freeman’s research shows people value immersive experiences (64%)—but only when they unlock learning (hands‑on activations, demos), commerce (samples/demos at booths), and meaningful expert conversations. A neon selfie wall won’t cut it if the sessions feel like recycled talking points. The lesson for fashion/apparel: design “wow” moments that are in service of discovery and deal flow—live sampling of near‑shore fabric finishing, a generative‑AI studio for speed‑to‑design, or a challenge where buyers and makers co‑prototype an upcycled capsule in 90 minutes. Make it beautiful; make it useful; make it authentic. Freeman report PDF21

A note on “cultural moments” and attendance volatility

Cultural festivals aren’t trade shows, but they’re instructive for audience expectations. In 2025, Essence Festival organizers and local media acknowledged pace‑behind ticket sales versus a record‑setting 2024 and lower hotel occupancy year‑over‑year—an example of how even beloved brands can face “moment fatigue” when the product feels less aligned to core audience desire. The message for B2B organizers is similar: culture drives draw, but only when the content and curation feel intimately tuned to the community’s identity and needs, not over‑manufactured for social optics. FOX 8 New Orleans22 Black Enterprise23

What content needs to evolve: three fast-moving frontiers to feature on stage and on the floor

AI and creative speed: 2024–2025 fashion outlooks flag generative AI moving from buzz to use cases—sketch expansion, fit imagery, demand sensing, and content atomization. The industry overall will grow modestly (2–4% top‑line in 2024), but AI can improve margin and cycle time—prime fodder for live demos and how‑to workshops that go beyond slides. McKinsey/BoF24

Virtual try‑on and returns: Online apparel returns hovered around 22% in early 2024, over three times the in‑store rate, with “did not fit” and “not as expected” as top reasons—exactly the problems VTO aims to reduce. Case studies (e.g., Avon in beauty) show conversion and AOV lifts with VTO; the fashion VTO stack is maturing fast enough to warrant live fittings, test booths, and post‑mortems on what fails. Retail TouchPoints25 Forbes26

Nearshoring and supply resilience: Mexico surpassed China as the U.S.’s biggest trading partner in 2023, underscoring the momentum for nearshore manufacturing—with caveats on labor, infrastructure, and policy risk. Shows that convene U.S., Mexico, and CAFTA‑DR partners for practical sourcing roadmaps, capacity tours, and compliance clinics will be more than talk—they’ll be deal rooms. BCG27

What’s working now: patterns from events that are growing or delivering ROI

Hosted buyer and curated matches: Outdoor Retailer’s 2024 pivot to a hosted buyer program brought buyers from 49 states, representing more than 30,000 retail locations, and a 3:1 buyer‑to‑brand ratio—high‑signal meetings that exhibitors can trace to orders. Outdoor Retailer18

Quality over quantity: Première Vision’s February 2024 edition was smaller year‑over‑year, but exhibitors raved about the value of conversations and “strong frequency” at stands. It’s a reminder that smaller can be better—if the right buyers show up and the agenda drives them to you. WWD14

International magnetism and editorial voice: CIFF’s integrated position with Copenhagen Fashion Week, its sustainability lens, and international buyer focus have expanded draw beyond the Nordics, helping it crack 20,000+ attendees. FashionNetwork17

Ecosystem density: NRF’s near‑40,000 attendance isn’t a mystery; it’s a flywheel of senior buyer density, broad vertical appeal, and an orbit of curated side events that make a trip to New York a guaranteed use of time. nrf.com3 Pivotree19

Community spotlights: how curated groups amplify connection

One reason NRF hums is the halo of private community dinners, salons, and bashes that make the week feel like a reunion with purpose. RETHINK Retail, for example, layered a private Fashion Innovation discussion (with Adobe’s AI fashion showcase), an AI in Retail Conference co‑hosted with Microsoft, a gala that pairs runway with robotics and startups, and an RSVP‑only Global Retail Leaders dinner—formats that blend learning, deal‑making, and culture. In Vegas, their Shoptalk Bash doubled down on high‑trust networking, drawing execs, partners, and experts into social settings where collaborations form. Curated micro‑communities like these can turn “going to the show” into “going to my community’s week,” which is a fundamentally stronger draw. RETHINK Retail28 RETHINK Retail29 RETHINK Retail30

The bottom line

Trade shows in fashion and apparel aren’t vanishing—they’re splitting into two camps. The ones that cling to old formulas and count selfies as success will likely keep shrinking. The ones that become high‑signal marketplaces and learning arenas—where brands land accounts, buyers discover next‑season edge, and communities feel seen—will thrive. The data shows attendance can be coaxed back when value is obvious; exhibitor space and buyer intent are already closer to 2019 than many think. If you build for commerce, candor, and community, the aisle won’t just be crowded; it’ll be consequential. CEIR1 TSNN2 Freeman report PDF21 nrf.com3

Works cited (inline above)

U.S. exhibition recovery and attendance dynamics: CEIR1, TSNN2, UFI12

Event case studies: MAGIC/PROJECT/SOURCING (Las Vegas) HKTDC Research13; Première Vision WWD14, The Spin Off15, GL events16; CIFF FashionNetwork17; Outdoor Retailer Outdoor Retailer18; NRF nrf.com3, Pivotree19

Social discovery: TikTok Ads9; Sprout Social10; HubSpot Blog11

Strategy and content themes: McKinsey/BoF State of Fashion 202424

Nearshoring: BCG27

Nike/adidas channel rebalancing: Retail Dive4; NIKE IR5; PYMNTS6; adidas-group.com7; Bloomberg8

Community formats: RETHINK Retail events at NRF28; Global Retail Leaders Dinner29; Shoptalk Vegas Bash30